2026 Geopolitical Arbitrage: Monetizing $18 Oil Risk Premium

Discover how institutional capital is monetizing 2026 Middle East escalation via $18 oil risk premiums, CHF carry trades, and 24/7 tokenized gold assets.

administrator

administrator

The 2026 Geopolitical Arbitrage: How Institutional Capital is Monetizing the Middle East Escalation

March 1, 2026. Missiles cross the night sky over the Middle East, and traditional financial markets are tightly shut for the weekend. Retail traders flood online forums, bracing for Monday’s opening bell with directional bets on oil and defense stocks. Institutional money managers take a vastly different path. They do not wait for the open. They execute.

Following the severe escalation of US-Iran military hostilities over the first weekend of March, global capital began a massive, orchestrated flight to safety. Real-time market data reveals a landscape where spot gold has shattered the $5,390 per ounce mark, and safe-haven currencies like the Swiss Franc (CHF) and US Dollar (USD) are aggressively absorbing emerging market outflows.

Retail traders buy the headline. Institutional desks buy the spread. Behind the chaos of the geopolitical strike, elite asset managers are actively pivoting to monetize the resulting geopolitical risk premium. They are leveraging deep-liquidity jurisdictions, exploiting cross-border yield spreads, and utilizing tokenized assets to bypass the constraints of traditional trading hours. The blueprint for trading global conflict has fundamentally changed.

Pricing the Chokepoint: The $18 Risk Premium

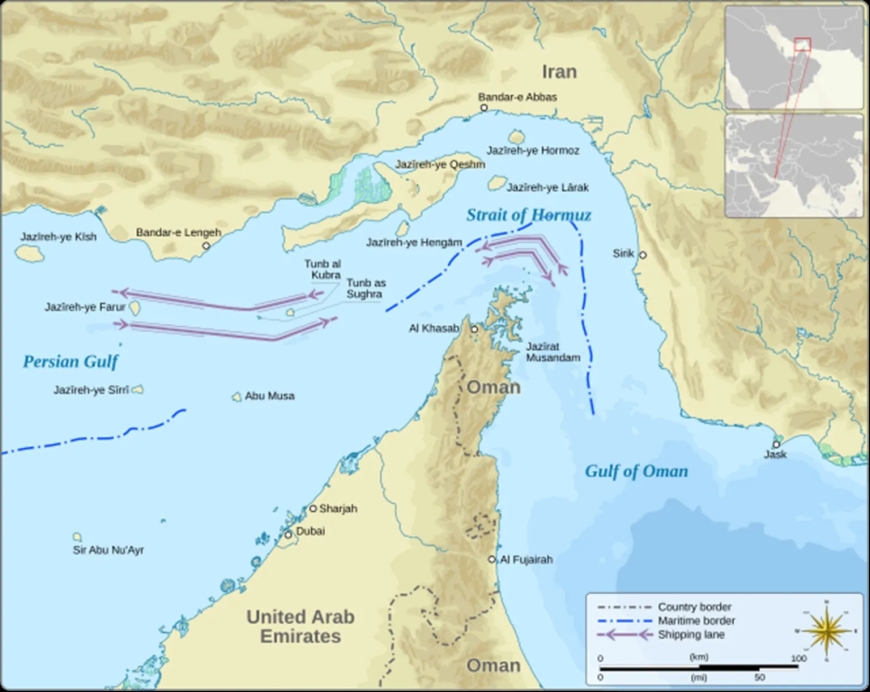

The immediate epicenter of current market volatility is not just the conflict itself, but the specific geography it threatens. The Strait of Hormuz handles roughly 20% of global oil transit. That equates to 15 to 20 million barrels of crude passing through a narrow, highly vulnerable maritime artery every single day.

When markets opened on March 2, Brent crude violently spiked 13%, hitting an intraday peak of $82 per barrel before settling near $77. This was not a speculative retail surge. It was a mechanical repricing of supply chain vulnerability.

Goldman Sachs analysts immediately injected an $18-per-barrel risk premium into their models, simulating the global economic impact of a potential six-week blockade of the Strait. Energy trading desks are not waiting to see if a blockade materializes. They are actively hedging against it. Implied volatility in Brent crude options has exploded, with heavy institutional monetization concentrated in the $85 to $90 call option strike range.

This environment elevates the strategic importance of physical energy proxies in the region. The United Arab Emirates serves as the physical and geopolitical fulcrum of this crisis. While Dubai and Abu Dhabi remain stable financial hubs, their infrastructure networks act as direct proxies for global energy supply risks. The Fujairah port, which sits outside the Strait of Hormuz on the Gulf of Oman, allows the UAE to bypass the chokepoint entirely via the Habshan–Fujairah oil pipeline. Institutional portfolios are heavily scrutinizing UAE infrastructure assets, viewing them as vital physical hedges against a prolonged US-Iran escalation.

The Silent Carry Trade: Harvesting Yield from Chaos

While the energy markets command mainstream attention, a much quieter, highly lucrative cross-border arbitrage is playing out across European and Asian liquidity hubs. Institutional managers are capitalizing on the massive influx of capital into safe-haven currencies to execute a nearly risk-free carry trade.

Switzerland currently operates as the ultimate deep-liquidity funding haven. The influx of frightened global capital has kept the Swiss Franc exceptionally strong, while the Swiss banking sector continues to offer ultra-low borrowing costs. Institutional clients and high-net-worth individuals are aggressively expanding their Lombard credit facilities—securing loans against their existing portfolios at rock-bottom rates of 0.5% to 1.0%.

The strategy requires a destination for this cheap capital. The US and the UK offer strictly regulated, high-quality sovereign debt that acts as the perfect yield generator. Managers are converting their borrowed Swiss Francs into British Pounds to purchase UK 10-year Gilts, which currently yield approximately 4.57%.

The math is brutally efficient. By borrowing at 1.0% and yielding 4.57%, institutions are capturing a gross spread of roughly 3.5% to 4.0%. The Bank of England’s current rate environment keeps Gilt yields highly attractive relative to mainland Europe. As long as geopolitical fears keep the Swiss Franc stable and borrowing costs low, this cross-border arbitrage remains one of the most profitable risk-adjusted trades in the 2026 financial landscape.

Weekend Safe Havens and the Tokenized Gold Rush

Geopolitical crises rarely adhere to the Monday-through-Friday schedule of traditional exchanges. When the US-Iran escalation accelerated over the March 1–2 weekend, legacy markets were offline. Spot gold (XAU/USD) would eventually spike over 2% at the Monday open to trade around $5,390 per ounce, driven by a desperate institutional flight-to-safety.

Capital cannot afford to sit idle for 48 hours during a military conflict. The weekend exposed a massive commercial demand for 24/7 safe-haven liquidity vehicles.

Tokenized gold assets became the immediate beneficiary of this structural market gap. PAX Gold (PAXG), a digital token backed by physical gold bullion, traded at a staggering 2.2% premium over the weekend. Asset managers and family offices utilized blockchain rails to secure gold exposure while the COMEX and London Bullion Market were closed. This premium serves as a glaring commercial signal: the institutional appetite for continuous, round-the-clock liquidity products is rapidly outpacing the capabilities of legacy financial infrastructure.

The Structural vs. Temporary Debate

The current market behavior reveals a sharp divergence in how different participants view the lifespan of this crisis. Retail trading forums are awash with emotional, directional bets. The prevailing sentiment among retail participants is a simplistic "long gold, long oil" strategy, reacting almost entirely to the visceral shock of weekend strike headlines.

Institutional notes from entities like UBP and Kpler paint a much more complex picture. The primary debate on elite trading desks is not about the immediate price action, but the duration of the geopolitical premium.

Historical precedent offers a mixed guide. Analysts are quick to point out that in previous conflicts—such as the 2020 US-Iran tensions following the death of Qasem Soleimani, or the initial shock of the 2022 Ukraine invasion—oil and forex spikes faded rapidly once the initial panic subsided. Capital returned to its baseline allocations within weeks.

The 2026 escalation is forcing a revision of those models. The direct, kinetic targeting of energy infrastructure has shifted the institutional consensus. Traders and risk analysts are issuing internal warnings that the current risk premium may become structural. If the Strait of Hormuz faces prolonged disruption, the $18-per-barrel premium modeled by Goldman Sachs will not evaporate. It will become a permanent fixture of the global energy supply chain, fundamentally altering inflation expectations and central bank rate paths for the remainder of the year.

Building the Next-Generation FX Rails

The massive volume of cross-border arbitrage currently flowing between Swiss funding hubs and UK yield destinations requires seamless, instantaneous execution. The legacy correspondent banking system, with its T+2 settlement times and high friction costs, is increasingly viewed as a liability during periods of extreme market volatility.

Singapore and Switzerland are actively engineering the solution. Both nations operate as politically neutral, deep-liquidity safe havens. Switzerland provides the cheap funding currency, while Singapore acts as the premier Asian foreign exchange routing hub. Together, they are pioneering the technological frontier for institutional arbitrage.

The Bank for International Settlements (BIS) recently concluded "Project Mariana," successfully testing automated cross-border FX settlements using wholesale Central Bank Digital Currencies (wCBDCs) between Switzerland, Singapore, and the Eurosystem.

The successful implementation of automated market makers (AMMs) in a heavily regulated, cross-border environment means the friction of the CHF-Gilt carry trade will eventually approach zero. Institutions will soon be able to execute complex, multi-jurisdictional arbitrage strategies instantly, 24 hours a day, without counterparty settlement risk. The weekend tokenized gold rush and the success of Project Mariana both point to the same inevitable conclusion: the future of geopolitical risk trading is entirely digital, continuous, and automated.

Snippet Answers

What is the CHF-Gilt carry trade? The CHF-Gilt carry trade is an institutional arbitrage strategy where investors borrow Swiss Francs via low-interest Lombard loans (0.5%–1.0%) and use the capital to purchase UK 10-year Gilts yielding around 4.57%. This generates a nearly 4.0% risk-adjusted spread, leveraging Swiss liquidity and British regulated yields.

How does the Strait of Hormuz affect oil prices? The Strait of Hormuz is a critical maritime chokepoint handling roughly 20% of global oil transit, or 15 to 20 million barrels daily. Threats of a blockade inject a massive risk premium into oil markets, with analysts currently pricing in an $18-per-barrel premium due to US-Iran military escalation.

Why did tokenized gold trade at a premium? During the March 2026 military escalation, traditional commodities markets were closed for the weekend. Institutional investors seeking immediate safe-haven assets utilized tokenized gold (like PAXG), driving its price to a 2.2% premium over spot gold due to the high demand for 24/7 liquidity outside legacy trading hours.

Frequently Asked Questions

Why are institutional managers using Swiss Lombard loans right now? Switzerland is a primary safe-haven jurisdiction, meaning global capital floods into the country during crises, keeping the Swiss Franc highly liquid. Swiss private banks offer Lombard loans—credit secured against an investor's existing portfolio—at ultra-low rates (0.5% to 1.0%). Institutions use this cheap capital to fund higher-yielding investments abroad without liquidating their core assets.

What makes UAE infrastructure a physical proxy for energy risks? The UAE relies heavily on the Strait of Hormuz for shipping, but it also possesses strategic bypass infrastructure. The Habshan–Fujairah oil pipeline allows the UAE to transport crude directly to the Gulf of Oman, bypassing the Strait entirely. As threats to the Strait increase, the strategic and financial value of Fujairah’s port and pipeline infrastructure surges, making it a critical hedge for energy portfolios.

How is the 2026 Middle East escalation different from 2020 or 2022 market shocks? Previous geopolitical shocks saw rapid spikes in oil and forex that faded as supply chains adapted. The 2026 escalation involves direct, kinetic threats to primary energy transit infrastructure. Institutional analysts warn this creates a "structural" risk premium, meaning elevated prices and volatility will persist long-term if shipping routes remain physically contested.

What is Project Mariana and why does it matter for FX trading? Project Mariana is an initiative by the Bank for International Settlements (BIS) testing the use of wholesale Central Bank Digital Currencies (wCBDCs) for cross-border foreign exchange. By using automated market makers between hubs like Singapore and Switzerland, it promises to eliminate settlement delays and counterparty risks, allowing institutions to execute arbitrage strategies instantly.

How are options markets pricing the current geopolitical crisis? Energy trading desks are aggressively buying Brent crude call options in the $85 to $90 strike range. Elevated implied volatility in these specific contracts indicates that "smart money" is actively hedging against a worst-case scenario, such as a multi-week blockade of the Strait of Hormuz, rather than just speculating on minor price fluctuations.

Closing Insight

Geopolitical crises expose the mechanical realities of global finance. While the broader public reacts to the immediate shock of military escalation, institutional capital treats conflict as a catalyst for structural realignment. The current environment—defined by $5,390 gold, $82 crude, and the relentless efficiency of the CHF-Gilt carry trade—demonstrates how rapidly deep-liquidity hubs adapt to global instability. As traditional market hours prove increasingly inadequate for modern crisis management, the shift toward 24/7 tokenized assets and automated cross-border settlements is no longer theoretical. It is the new baseline for institutional risk management.